Real decisions are easier to see through examples. These are illustrative, not advice for any specific person.

A. HDB upgrader with young children. Concerns: school timing, space, ABSD, renovation, a possible rental gap.

How to think: if space and timing matter most, a resale unit — or a new launch that’s close to TOP — often fits better than a project that’s years away.

Sequence the HDB sale carefully around the ABSD window.

B. Young couple, no urgent move-in need. Concerns: budget, PPS, future planning.

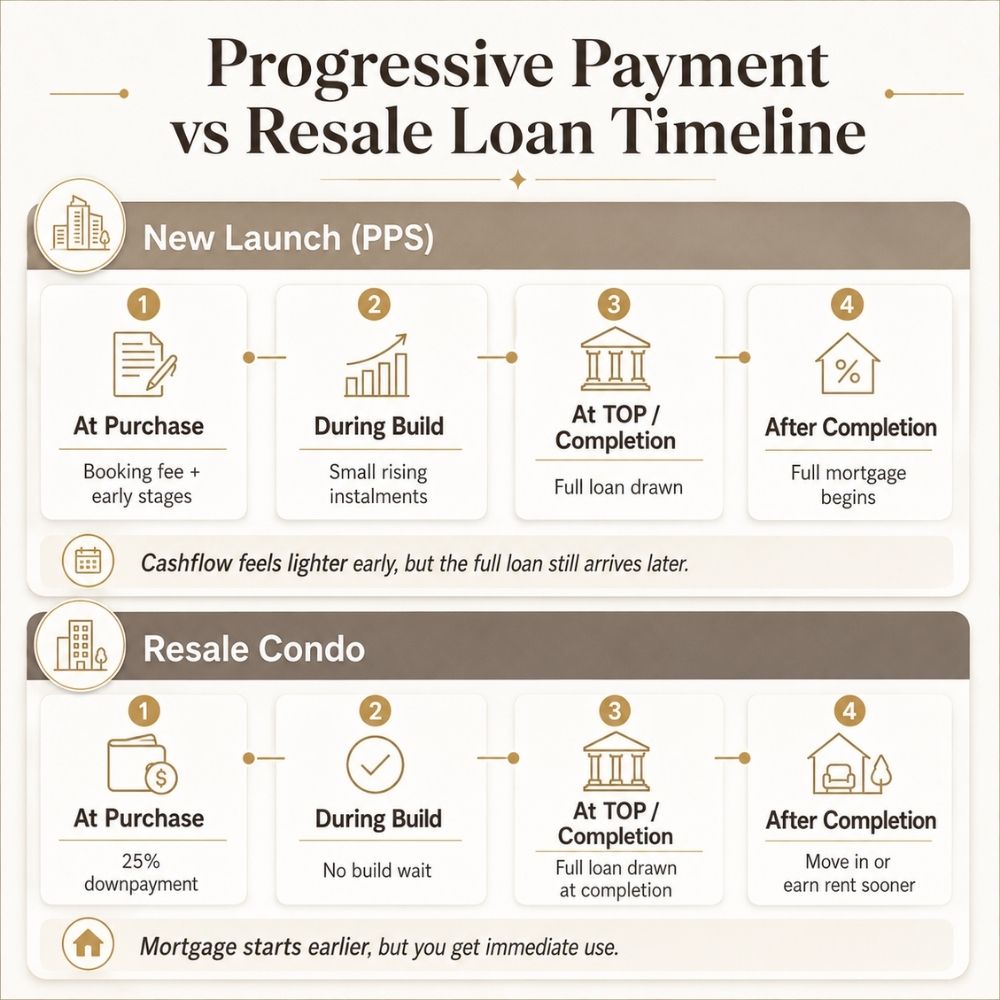

How to think: a new launch can suit you well if cashflow and holding power are steady and you’re comfortable waiting.

The staged payments give you breathing room.

C. Investor. Concerns: rental yield, ABSD, vacancy, the TOP wait, future resale liquidity.

How to think: resale can start earning rent immediately, but weigh the 20% ABSD (for a second property), older-building risks and the rising completion pipeline.

A new launch means no rental income until TOP.

D. Rightsizer / downsizer. Concerns: convenience, proximity to family and medical care, low maintenance.

How to think: resale often gives certainty and immediate use, with freedom to pick the exact size.

A near-TOP new project can also work if you don’t need to move right away.

E. Lower-PSF resale vs higher-PSF new launch. Concerns: which is really “cheaper.” How to think: go back to Section 4.

Compare total quantum and liveable layout, not headline PSF.

You are right, there is always a good friend/bro that likes to give ‘advise’ base on own opinions, LOL. Great that i came across this article. Will be in contact after CB. Thanks