PrimeKey Analysis Singapore: A Property Analysis Tool for Smarter Condo Shortlisting

Buying a condo in Singapore is rarely just about the lowest PSF, the nicest showflat, or the most convincing sales pitch.

Those things may catch your attention.

But they do not always tell you whether a property will stay easy to rent, easy to resell, and comfortable to hold years from now.

That is where PrimeKey Analysis can help.

PrimeKey Analysis is a property analysis tool that compares condos based on key fundamentals such as MRT access, URA growth areas, Government Land Sales pipeline, project size, remaining tenure, rental yield, nearby primary schools, and HDB upgrader demand.

It gives buyers a more structured way to compare properties.

But a strong property score is not the same as a strong property decision.

PrimeKey can analyse the property.

Whether that property fits your life, your numbers, your family, and your timeline is a separate question.

That is why I treat PrimeKey Analysis as one part of a wider condo shortlisting process — not the only deciding factor.

Table of Contents

Quick Answer: What Is PrimeKey Analysis in Singapore Property?

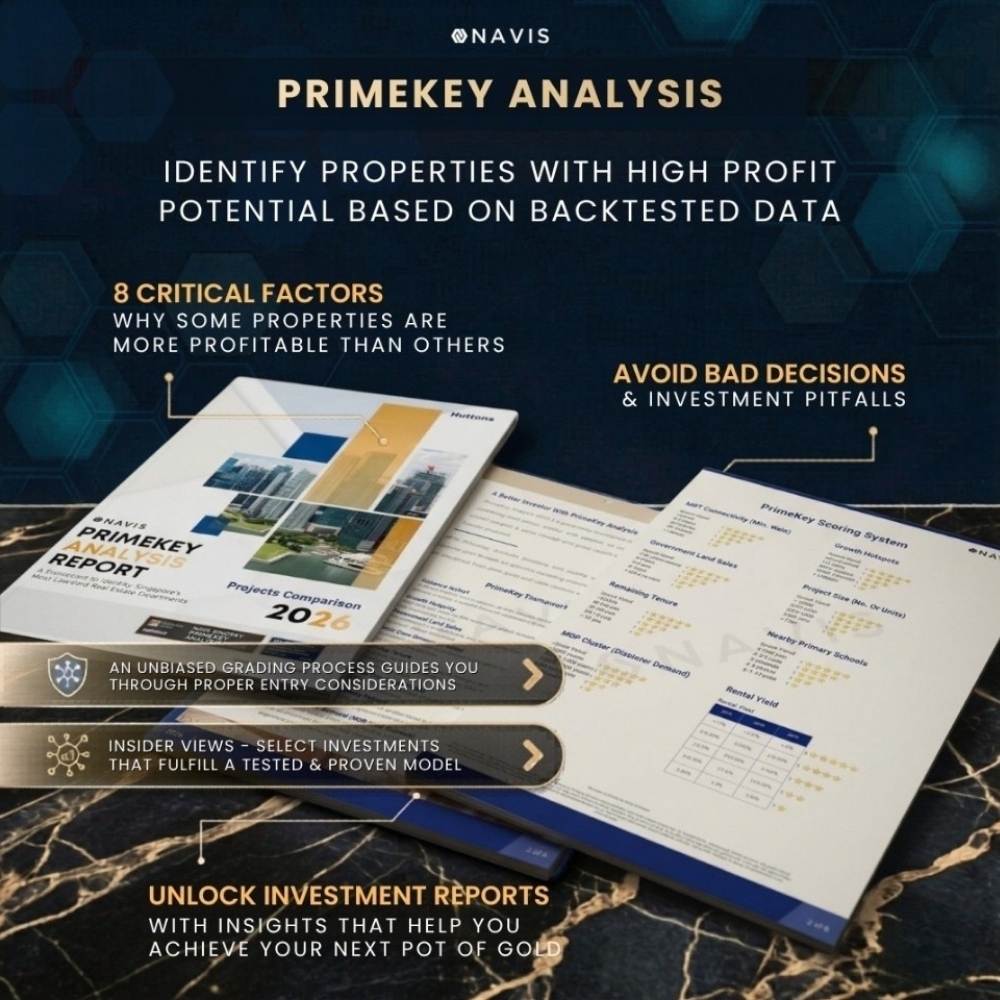

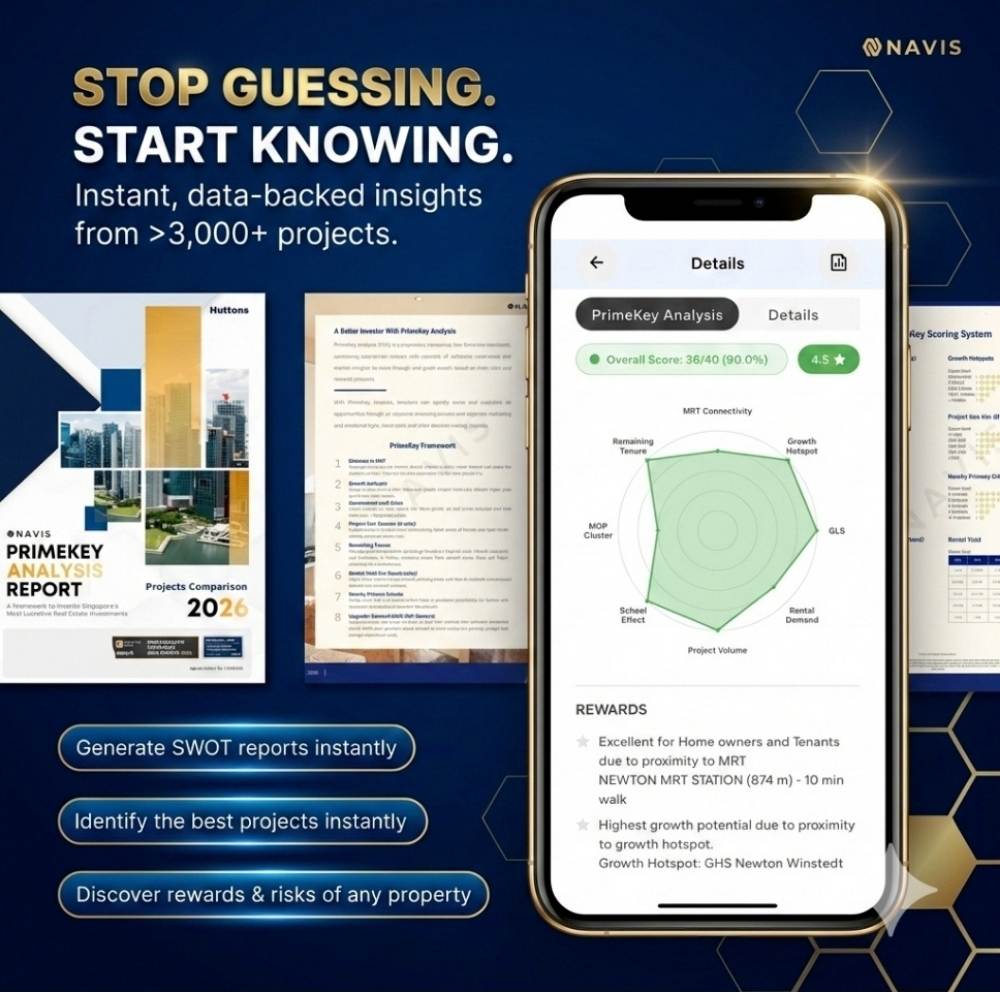

PrimeKey Analysis is a data-driven property scoring system within the Navis Atlas platform.

It reviews Singapore condos and private residential projects across eight fundamentals — MRT access, URA growth areas, Government Land Sales pipeline, project size, remaining lease, rental yield, nearby primary schools, and HDB upgrader demand — and turns them into a comparable score.

The score helps buyers compare condo fundamentals more objectively.

It does not assess your financial readiness, CPF position, lifestyle needs, or exit timeline, which still need to be reviewed separately before you decide.

Why Price and PSF Alone Are Not Enough

Most buyers start with price: Is this PSF reasonable? Is it cheaper than the new launch nearby? Is this a good entry price?

Fair questions — but price alone doesn’t tell the full story.

A lower PSF can still come with weaker tenant demand, a shorter lease runway, or a thinner future buyer pool.

A higher PSF can still make sense when the project has better transport, healthier transaction volume, and a more realistic exit.

When you buy a condo, you’re not only buying today’s unit — you’re buying into the location’s future demand, its likely rental pool, the eventual resale buyer, and the financial weight you’ll carry along the way.

PrimeKey helps with the property side of that picture.

The buyer side still matters, and that’s the part most comparison tools leave out.

What Is PrimeKey Analysis?

PrimeKey Analysis is a structured property analysis tool for comparing Singapore condos against a consistent set of fundamentals.

Instead of relying only on gut feel, sales talk, or simple PSF comparison, PrimeKey reviews each project across eight factors that may influence long-term demand, rentability, resale appeal, and holding strength.

The logic is straightforward.

A property should not be judged only by how attractive it looks today.

It should also be reviewed by what may support or weaken demand over time.

So PrimeKey works less like a final verdict and more like a consistent lens.

It helps you compare projects on the same terms before asking the more personal question:

Even if this is a strong property, is it right for me?

PrimeKey Analysis Singapore

The 8 PrimeKey Factors Used to Compare Condo Projects

PrimeKey Analysis looks at property-level signals that may affect own-stay comfort, rental appeal, resale visibility, and future buyer demand in Singapore’s private residential market.

The eight PrimeKey factors are MRT access, nearby primary schools, project size, rental yield, URA growth areas, nearby Government Land Sales sites, remaining tenure, and the nearby HDB MOP upgrader pool.

| Factor | What It Means | Why It Matters | Most Relevant For |

|---|---|---|---|

| Distance to MRT | What It Means How accessible the project is to MRT transport. | Why It Matters Wider tenant and buyer pool, daily convenience, and stronger resale appeal. | Most Relevant For Own stay Investment Exit |

| Nearby Primary Schools | What It Means Schools within the relevant nearby radius. | Why It Matters Supports owner-occupier demand from families. | Most Relevant For Own stay Exit |

| Project Size | What It Means Total number of units in the development. | Why It Matters Larger projects may offer more facilities, more transactions, and stronger resale visibility. | Most Relevant For Own stay Investment Exit |

| Rental Yield of the Area | What It Means Rental income relative to property value. | Why It Matters Signals tenant demand and holding strength. | Most Relevant For Investment |

| URA Growth Hotspots | What It Means Areas with long-term planning or transformation potential. | Why It Matters May support future demand if planning translates into real improvement. | Most Relevant For Own stay Investment |

| Upcoming GLS Nearby | What It Means Government Land Sales sites around the area. | Why It Matters New land prices and launches may influence future price benchmarks. | Most Relevant For Investment Exit |

| Remaining Tenure | What It Means How much lease remains on the property. | Why It Matters Affects financing, CPF usage, buyer pool, and resale appeal. | Most Relevant For Investment Exit |

| Nearby HDB MOP Upgrader Pool | What It Means HDB flats nearby reaching Minimum Occupation Period. | Why It Matters A future pool of upgraders may support nearby private home demand. | Most Relevant For Exit |

Property Fit vs Personal Fit

What PrimeKey Measures — and What Still Needs Personal Review

PrimeKey can support condo shortlisting, but the final decision should still consider your CPF, cash flow, family needs, renovation budget, emotional comfort with debt, and sell-buy timeline.

| PrimeKey Helps Analyse | PrimeKey Does Not Analyse |

|---|---|

| PrimeKey Helps Analyse The property’s fundamentals | PrimeKey Does Not Analyse Your real reason for buying |

| PrimeKey Helps Analyse MRT distance, nearby schools, tenure, rental yield, GLS sites, URA planning areas, project size, and upgrader demand | PrimeKey Does Not Analyse Your family’s lifestyle needs |

| PrimeKey Helps Analyse How one Singapore condo project compares with another | PrimeKey Does Not Analyse Your CPF position and cash comfort |

| PrimeKey Helps Analyse Potential demand drivers around a project | PrimeKey Does Not Analyse Your renovation budget and emergency buffer |

| PrimeKey Helps Analyse Property-level strengths and weaknesses | PrimeKey Does Not Analyse Your emotional comfort with debt |

| PrimeKey Helps Analyse Future resale and rental appeal indicators | PrimeKey Does Not Analyse Your sell-buy timeline and fallback plan |

The 8 PrimeKey Factors in Simple Buyer Language

The eight PrimeKey factors can be grouped into three main jobs:

- Livability

- Investment and holding strength

- Exit and resale demand

This grouping matters because buyers do not all want the same thing.

An investor may focus more on rental yield and tenant pool.

A family may care more about MRT access, schools, layout, and daily convenience.

An HDB upgrader may need to think harder about future resale liquidity, CPF planning, and whether there will be a realistic buyer pool when it is time to exit.

One factor rarely tells the whole story.

A unit beside an MRT station but with a short remaining lease may still see its buyer pool narrow over time.

A project set back from the MRT but near future transformation plans, with healthy size and a steady upgrader pool, may still deserve a closer look.

A nearby GLS site can reset price benchmarks if new launches sell higher — but that’s not automatic; it depends on supply, demand, timing, and the price you enter at.

PrimeKey Analysis Singapore

What PrimeKey Analyses Well — and What It Does Not

PrimeKey Analysis helps compare Singapore condo projects by looking at property-level fundamentals. It can organise the project comparison, but it should not replace a personal affordability, CPF, lifestyle, and timeline review.

In simple terms, PrimeKey is useful for shortlisting properties. The final decision still depends on whether the property fits your family, cash flow, CPF position, risk comfort, and next-home timeline.

| PrimeKey Helps Analyse | PrimeKey Does Not Analyse |

|---|---|

| PrimeKey Helps Analyse The property’s fundamentals | PrimeKey Does Not Analyse Your real reason for buying |

| PrimeKey Helps Analyse MRT distance, nearby schools, tenure, rental yield, GLS sites, URA planning areas, project size, and upgrader demand | PrimeKey Does Not Analyse Your family’s lifestyle needs |

| PrimeKey Helps Analyse How one Singapore condo project compares with another | PrimeKey Does Not Analyse Your CPF position and cash comfort |

| PrimeKey Helps Analyse Potential demand drivers around a project | PrimeKey Does Not Analyse Your renovation budget and emergency buffer |

| PrimeKey Helps Analyse Property-level strengths and weaknesses | PrimeKey Does Not Analyse Your emotional comfort with debt |

| PrimeKey Helps Analyse Future resale and rental appeal indicators | PrimeKey Does Not Analyse Your sell-buy timeline and fallback plan |

PrimeKey is useful because it organises the property side of the decision.

It can help you compare:

- location fundamentals

- rental demand signals

- project scale

- lease runway

- nearby buyer pools

- supply and growth factors

- resale and rental appeal indicators

Without a framework, buyers often compare projects in a messy way.

One looks cheaper.

One looks newer.

One feels more luxurious.

One has a stronger sales story.

PrimeKey helps put the comparison into a more consistent format.

But it does not measure everything.

A property can look strong on paper and still feel tight every month.

It can score well for yield and still be wrong for an own-stay family.

The score helps us understand the property.

The planning helps us understand whether the property fits your life, your numbers, and your next move.

Rick’s 4-Layer Property Fit Framework

When I use PrimeKey Analysis with buyers, I do not start and end with the score.

I place it inside a wider property planning process.

The four layers are:

- Buyer Fit

- Financial Fit

- Timeline Fit

- Property Fit

PrimeKey sits inside the Property Fit layer.

But I usually read it together with the buyer’s needs, numbers, and timeline, so the score has proper context.

Layer 1: Buyer Fit

This layer is about you, not the condo.

Why are you buying now — own stay, investment, an upgrade, a school zone, a retirement reset?

What would make you regret this purchase three years later?

How much do space, privacy, commute, and family support matter, and can you hold calmly if the market slows?

Different buyers need different properties, so the same PrimeKey score can mean different things to each of them.

That’s why buyer fit comes first.

Layer 2: Financial Fit

This is where many buyers should slow down.

The bank may tell you how much you can borrow.

It does not tell you how much you should borrow.

A proper financial fit review should look at:

- available CPF Ordinary Account funds

- cash required for downpayment

- Buyer’s Stamp Duty

- Additional Buyer’s Stamp Duty, if applicable

- legal fees

- renovation and furnishing budget

- monthly repayment comfort

- emergency buffer

- existing debts

- income stability

- holding power if rates or circumstances change

For HDB upgraders, CPF planning is especially important.

Selling your HDB may involve refunding the CPF principal used, accrued interest, and any housing grants used with accrued interest where applicable.

This does not mean the money is lost.

But it affects how much sale proceeds return to CPF and how much cash you may have for the next move.

So the question is not only:

“Can I qualify?”

The better question is:

After all costs, CPF refunds, loan repayments, and monthly obligations, does this move still feel steady?

If the answer is no, the property may be strong, but the plan may need adjustment.

Layer 3: Timeline Fit

Property decisions are not only about what to buy.

They are also about when and how the move is executed.

This matters especially for HDB owners upgrading to private property.

Some common timeline questions include:

- Should you sell first or buy first?

- Do you need temporary housing?

- Will you need an extension of stay?

- Are you prepared for ABSD upfront if you buy first and qualify for remission later?

- What happens if the sale takes longer than expected?

- What happens if the renovation timeline stretches?

- What is your realistic holding period?

- Who is your likely buyer when you eventually exit?

A property may have strong fundamentals.

But if the sequence is wrong, the buyer may face cashflow pressure, rushed decisions, or uncomfortable transition gaps.

Sometimes, the right property at the wrong time becomes the wrong move.

Layer 4: Property Fit — Where PrimeKey Comes In

Once the first three layers are understood, PrimeKey Analysis becomes more useful.

The question shifts from:

Which condo scores highest?

To:

Which condo has strong fundamentals that also fit this buyer’s purpose, budget, and timeline?

If you are buying for rental income, we may pay closer attention to MRT access, rental yield, tenant demand, and exit liquidity.

If you are buying for family own stay, we may look harder at schools, layout, project environment, daily convenience, and whether the location supports your family routine.

If you are upgrading from HDB, we may check whether the future buyer pool is wide enough, whether the quantum is realistic, and whether you can hold long enough for the plan to work.

PrimeKey gives the property score.

Your profile tells us how to read it.

Same Condo, Two Buyers, Different Decision

Picture a condo that scores strongly under PrimeKey: a large development beside an MRT interchange, with healthy rental demand, strong transaction volume, and a wide tenant pool.

On paper, it looks attractive. The decision still depends on the buyer.

Buyer A — the investor. Single, in their 30s, focused on rental demand and resale liquidity.

The large project size supports transaction visibility, the MRT access supports tenant demand, and the yield gives some income support.

Here, the score and the goal point in the same direction.

Buyer B — the upgrading family. A couple moving from an HDB flat with elderly parents at home.

They want space, a quieter environment, and a repayment that doesn’t stretch them.

The same project may feel too busy, the unit too tight, the quantum too heavy on their cash buffer.

The property is still fundamentally strong; it just isn’t the right fit.

Same condo. Same score. Different buyer, different decision. The score supports the conversation — it doesn’t replace it.

How to Read a PrimeKey Score in Context

A PrimeKey score is a useful starting point, not a final verdict.

A strong score suggests healthier fundamentals, but it doesn’t mean you should automatically buy.

Can you afford it comfortably, does it suit your family, is the holding period realistic, and do you understand the exit?

A strong property can still become stressful if the buyer is overextended.

A moderate score usually signals trade-offs rather than a wrong choice.

The real question is whether those trade-offs matter to you.

Weaker on yield but buying for long-term own stay? That may not bother you.

Weaker on MRT access but the price reflects it and you drive daily?

Possibly workable.

A weak score is a reason to slow down, not an automatic rejection.

You may still proceed with a clear personal reason, a suitable price, or a long-term plan that makes sense — but don’t wave away the risks.

A weak score is a signal to ask better questions.

A Practical Condo Shortlisting Process

A simple way to use PrimeKey Analysis for condo shortlisting in Singapore:

Step 1 — Filter with PrimeKey.

Compare your shortlisted condos on fundamentals to see which projects are stronger, where the weaknesses sit, and which deserve a deeper look.

Instead of “this one feels nicer,” you can ask, “what’s driving the score?”

Step 2 — Confirm the fit.

Run the shortlist through Buyer Fit, Financial Fit, Timeline Fit, and Property Fit.

This is where the real decision happens, because the best property isn’t always the highest-scoring one — it’s the one that fits your goal, budget, family, and ability to hold or exit when needed.

Data helps you compare. Planning helps you decide.

Final Thoughts: Data Helps You Compare, Planning Helps You Decide

PrimeKey Analysis gives structure to condo comparison in Singapore.

It helps you move past price, PSF, and showroom impressions, and see which projects carry stronger fundamentals and which carry more trade-offs.

But the score isn’t the whole decision.

A property still has to fit the person buying it — your family, your CPF and cash position, your monthly comfort, your timeline, and your exit.

Sometimes the highest-scoring condo isn’t the most suitable one, and a quieter option fits your life better.

Wherever you are in the journey — just starting to think it through, working out your buyer, financial and timeline fit, or already comparing a few condos or holding a PrimeKey report — tell me where you stand. I’ll help you review whether a property fits your needs, numbers, timeline and next move before you commit.

PrimeKey Analysis FAQ

Frequently Asked Questions About PrimeKey Analysis Singapore

These questions explain how PrimeKey Analysis can support Singapore condo shortlisting, and where a personal property planning review is still needed.

PrimeKey Analysis is useful for comparing property fundamentals such as MRT access, tenure, project size, rental appeal, URA planning areas, GLS supply, nearby schools, and HDB upgrader demand. It helps you shortlist better, but it does not replace a review of your CPF, cash flow, family needs, and sell-buy timeline.

What is PrimeKey Analysis in Singapore property?

PrimeKey Analysis is a property scoring framework used to assess Singapore condos and private residential projects across fundamentals like MRT connectivity, URA growth areas, the GLS pipeline, project size, remaining tenure, rental yield, nearby primary schools, and HDB upgrader demand. It helps buyers compare projects in a structured way instead of relying only on price, PSF, or showroom impressions.

What are the 8 PrimeKey factors?

The eight PrimeKey factors are distance to MRT, remaining lease tenure, nearby HDB MOP upgrader pool, upcoming Government Land Sales nearby, URA growth hotspots, project size, rental yield of the area, and nearby primary schools. Together, they help assess livability, rental appeal, resale strength, and long-term demand drivers.

Is a high PrimeKey score enough to decide on a condo?

No. A high PrimeKey score may point to stronger property fundamentals, but it does not mean the condo suits every buyer. You still need to review your financial comfort, CPF position, family needs, renovation budget, timeline, and exit plan. The score informs the decision; it does not make the decision for you.

What does PrimeKey Analysis not measure?

PrimeKey Analysis does not measure your personal situation. It does not assess your cash buffer, CPF refund position, comfort with debt, family priorities, renovation budget, sell-buy timeline, or future life plans. These should be reviewed separately before deciding whether a property fits your overall plan.

Is PrimeKey Analysis only for investors?

No. PrimeKey Analysis can be useful for both investors and own-stay buyers. Investors may focus more on rental yield, tenant demand, and resale liquidity. Own-stay buyers may focus more on MRT access, nearby schools, environment, and long-term livability. The same score can be read differently depending on your objective.

How does CPF affect condo shortlisting in Singapore?

Your available CPF Ordinary Account balance, CPF used in your current property, accrued interest, and future usage rules all shape your real budget. For HDB upgraders, cash proceeds from a sale can differ from paper profit once CPF refunds and outstanding loans are settled. Reviewing your CPF position early helps you shortlist within a realistic range.

What is TDSR and why does it matter?

TDSR, or Total Debt Servicing Ratio, limits how much you can borrow by measuring your total monthly debt against income. Even if you qualify for a certain loan, the repayment should still feel manageable after household expenses, renovation costs, and emergency savings. Always verify the current TDSR threshold with MAS, your bank, or your mortgage adviser before committing.

Should an HDB upgrader sell first or buy first?

It depends on your finances, risk comfort, and timeline. Selling first gives a clearer view of your sale proceeds and reduces some uncertainty, but it may create a transition gap. Buying first can reduce disruption, but it adds financial pressure and may involve ABSD considerations. The right sequence should be planned before you commit.

Why does HDB MOP upgrader demand matter?

HDB owners reaching their Minimum Occupation Period may form part of the future private buyer pool. A condo near a large upgrader catchment may see steadier resale demand. However, this still needs to be checked against the price gap, affordability, location appeal, competing supply, and market conditions when you eventually sell.

Can PrimeKey Analysis predict property profit?

No tool can guarantee profit or predict returns with certainty. PrimeKey Analysis can highlight stronger or weaker fundamentals using structured factors, but future performance depends on entry price, market cycle, policy changes, interest rates, holding period, buyer demand, rental demand, and your own financial position.

What My Clients Say | Genuine Experiences

Real stories, real experiences—because your journey deserves nothing less than the best.

Awards and Accolades

Self Introduction

Hi, I’m Rick Long,

Associate Senior Division Director, Huttons Asia · CEA Reg. R026818Z

With decades of experience in Singapore’s real estate market, I’ve had the privilege of being mentioned in media outlets such as Channel NewsAsia, The Straits Times, and 99.co.

Over the years, I’ve written extensively on the local property landscape — tackling the real questions buyers and sellers face, and helping them navigate each step with greater steadiness and confidence.

Many of my clients have become long-time friends — their trust and kind reviews continue to inspire me to raise the bar in everything I do.

I believe real estate should be strategic, seamless, and deeply aligned with your life’s journey.

Related Articles:

Ever wonder if you are suitable for Sell one buy two investment concept? – Read more (Sell one buy two)

Is buying new launch or resale condo have better returns? – Read more (New Launch vs Resale condo)

Looking to upgrade from Hdb to condo? – Read more (Sell Hdb buy condo)

What to take note when selling Hdb resale flat? – Read more (Hdb Resale Process)

Buying another Hdb flat, and using the fund from current home? – Read more (Hdb contra)

Why do some Hdb flat price depreciate so much? – Read more (Hdb depreciation curve)

What is one of the most common reason for property negative sales? – Read more (Cpf accrued interest)

Financial calculation for selling a Hdb flat? – Read more (Hdb resale calculator)

Buying EC before selling your HDB? – Read more (Upgrade to EC before selling your HDB)

Should you sell your EC after 5 years? – Read more (Selling EC)