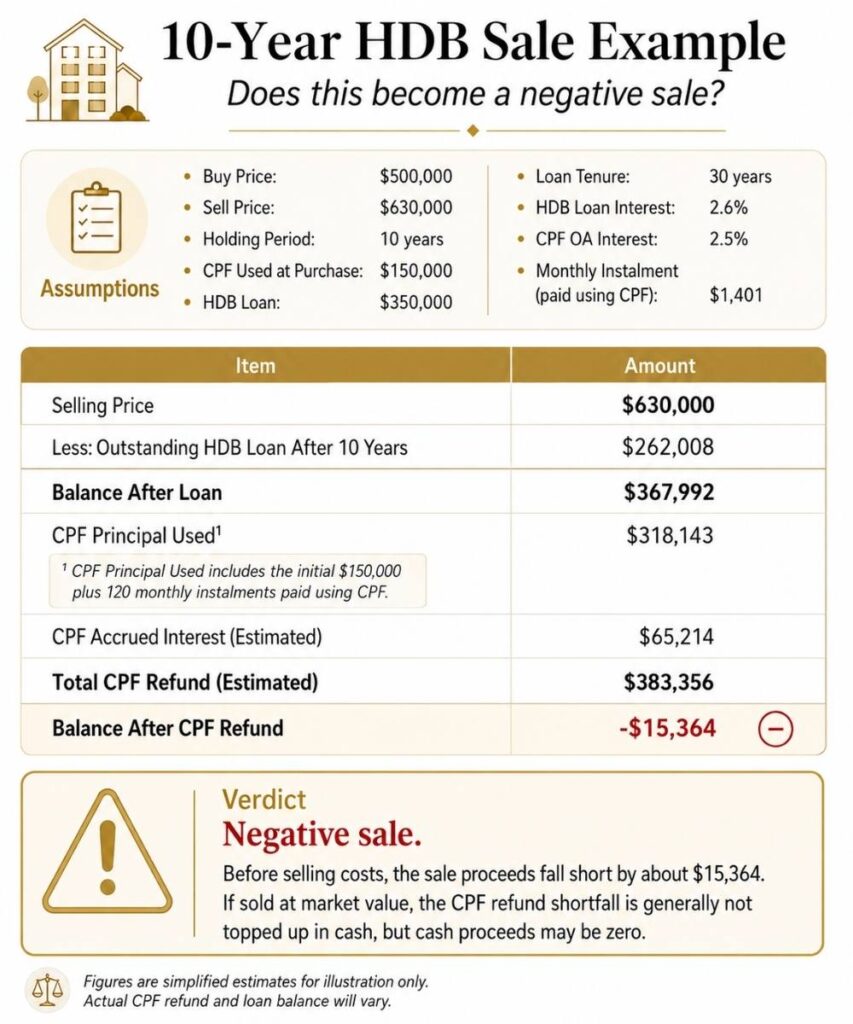

At first glance, it looks like:

“Bought at $400,000, sold at $650,000, so we made $250,000.”

But the cash in hand is closer to $180,000.

That does not mean the flat did badly.

It also does not mean CPF accrued interest “ate the gain”.

The $275,000 returned to CPF, made up of CPF principal used and accrued interest, goes back into their own account. It may support the next home or retirement, subject to CPF rules.

Their real position is not just cash.

It is:

$180,000 in estimated cash proceeds + $275,000 restored to CPF

That is a very different story from looking at paper gain alone.

This is why it pays to run the numbers before finding a buyer, not only after accepting an offer.

Can i check how do i know if i can afford to upgrade even i find that my flat is depreciating?

Hi Pauline, thanks for reading our article. The key is by doing an in-depth financial calculation. If upgrading is your priority, we will assess the options available after calculation. And we will provide proven methods and steps on how to go about it. Keep in touch, already send you an email. Thanks