Sell HDB, Buy Condo in Singapore: What to Know Before You Upgrade

A $1,000,000 HDB sale does not mean $1,000,000 reaches your bank account.

That one line is where many upgrade plans should begin.

Because selling your HDB to buy a condo in Singapore is not really just a housing upgrade.

It is a financial restructuring decision.

You are moving money, debt, CPF, timing and family plans all at once.

Get the sequence right, and the move can be made on steadier ground.

Get it wrong, and the cost tends to show up in places owners did not expect — CPF refund, accrued interest, ABSD, temporary accommodation, monthly repayment, or a cash buffer that suddenly feels thin.

This guide is for HDB owners who are seriously thinking about selling their flat and buying a condo in Singapore.

Not to push you to upgrade.

Just to help you see whether the move fits your numbers, your timeline, your family and your next stage of life.

Table of Contents

Why HDB Owners Consider Selling HDB to Buy Condo

For some, it is space — the family has grown, the children need their own rooms, and working from home has changed how the place is used.

For others, it is location: closer to parents, schools, work, or an MRT line that fits daily life better.

Some want more privacy or facilities. Some are thinking further ahead about their long-term property plan and whether moving from public housing to private makes sense for them.

Every reason here is valid. Each one still has to survive the numbers.

Most owners I meet are not chasing a condo. They are trying to give their family a little more room to breathe — without trading away their peace of mind to do it.

A condo offers a different lifestyle, but it also carries a different cost structure: a higher monthly repayment, maintenance fees, property tax, renovation, and a bank loan in place of an HDB loan.

The better question is not “Can I upgrade?”

It is “Will this still feel comfortable once the sale, CPF refund, loan redemption, purchase costs and monthly repayment are all mapped out?”

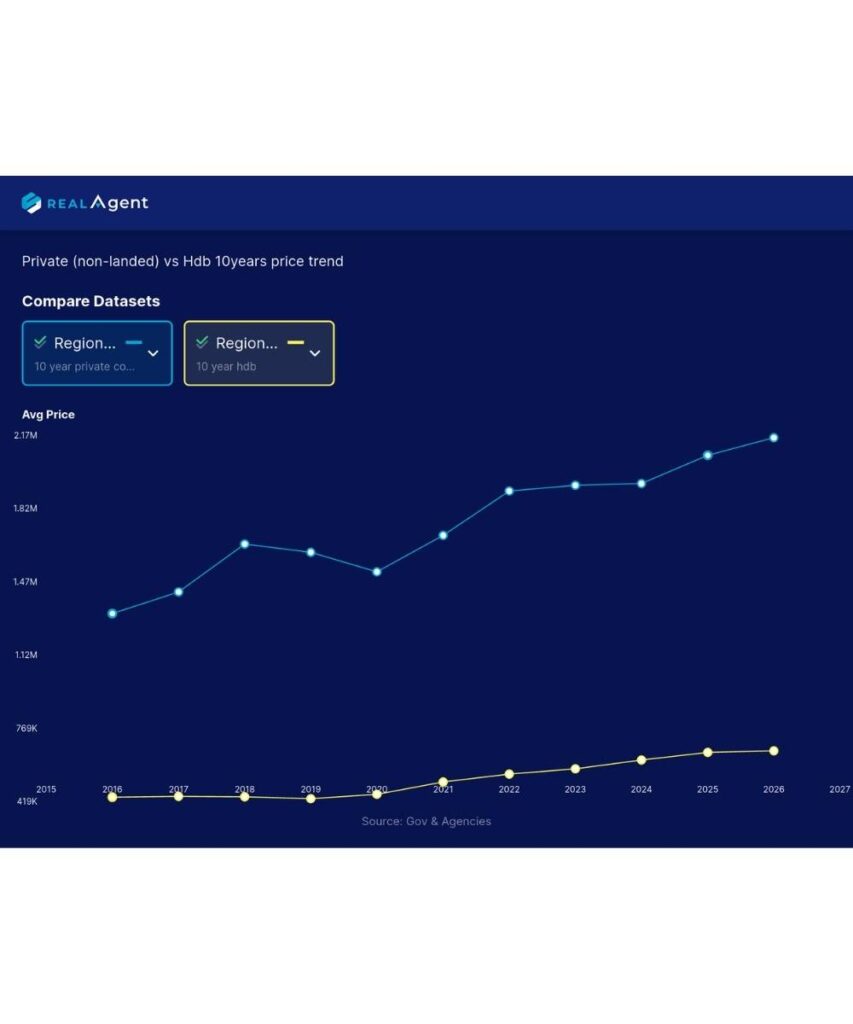

Is the Gap Between HDB and Condo Prices Widening — and Should That Rush You?

Simple answer: Over the past decade, private home prices have generally risen faster than HDB resale prices, so the gap between them has widened.

That is a fair thing to weigh. But a past trend is not a promise about the future, and recent supply shifts make the next few years genuinely uncertain.

Let the gap inform your plan — don’t let it rush it.

Some owners look at how far private prices have pulled ahead of HDB resale and feel a quiet pressure: if I don’t move now, will the jump only get bigger later?

It is an understandable worry, and it deserves a real answer rather than a brush-off.

Here is the honest version. Across the last several years, private non-landed prices have tended to climb faster than HDB resale, which has widened the absolute gap an upgrader needs to cross.

You can track the real figures yourself through URA’s Private Residential Property Price Index and HDB’s Resale Price Index — the official sources, rather than any single agent’s chart.

But the same data carries a second message that the urgency story tends to leave out.

A gap that widened over the past decade does not guarantee it keeps widening.

More recently, HDB resale price growth has cooled, and a sizeable wave of flats reaching MOP and completion is expected over the next few years — adding both choices for buyers and competition for sellers on the public-housing side.

Where the gap goes from here is not something anyone can promise.

So I would treat the widening gap as a consideration, not a starting gun.

Moving earlier to “beat the gap” still means taking on a larger, more leveraged purchase sooner — and that only helps you if the cash, CPF and monthly repayment also feel comfortable today.

If your numbers work, the gap is one more reason to plan the move properly and not drift.

If your numbers don’t work, no market trend makes a stretched move safe.

For more on how HDB values move over time, our HDB depreciation curve guide is worth a read alongside this.

Decision rule: A widening price gap can be a reason to plan earlier — not a reason to buy before your numbers are ready. The right time to upgrade is set by your finances and your family, not by a price index.

Can You Sell Your HDB Yet? MOP and Eligibility First

Before viewing condos or working out a new loan, check the first gate: can your flat even be sold yet?

Most owners can only sell after fulfilling the Minimum Occupation Period.

For many standard flats, the MOP is usually 5 years.

For newer Plus and Prime flats, it is generally longer, at 10 years.

The exact position depends on your flat type, purchase scheme and circumstances — so don’t rely on memory.

Confirm your actual eligibility with HDB.

This matters even more if you are planning around school admission, renovation timing, or the completion date of your next home.

If the MOP date is still ahead, that waiting time is not wasted — it is the calm window to prepare your numbers, timeline and shortlist.

What is MOP? HDB MOP means Minimum Occupation Period. It is the period you must fulfil — living in the flat — before you can sell your HDB on the open market. Usually 5 years for standard flats and 10 years for Plus and Prime flats. Confirm yours with HDB.

How Much Cash Will You Actually Get After CPF Refund?

This is the section that surprises the most owners.

Simple answer: Your HDB sale price is not your cash. You first settle the outstanding loan, refund the CPF you used plus accrued interest, and pay selling and legal costs.

The CPF portion returns to your CPF account, not your bank. Only the remainder reaches you as cash.

It is easy to look at the gap between what you paid and what you sell for and feel the gain is large. But after the loan is redeemed and CPF is refunded, the cash actually available is often much lower.

Here is an illustrative example.

Illustrative $1 Million HDB Sale Example

A $1,000,000 HDB sale does not mean $1,000,000 reaches your bank account. The sale proceeds must first settle the housing loan and CPF refund.

So the same sale reads three different ways:

Looks like: $1,000,000 sale price

Estimated gross cash proceeds: about $340,000 before miscellaneous selling costs

Returned to CPF OA: about $380,000

That distinction matters.

The CPF refunded to your Ordinary Account may be usable for your next home, subject to CPF rules — but it is not cash for every cost.

Things like the option fee, part of the down payment, renovation, moving, temporary accommodation and your emergency buffer often need actual cash.

What is CPF accrued interest?

CPF accrued interest is the interest your CPF savings would have earned if you had not used them for the flat.

It is not a penalty.

But it compounds over time, so the longer and more CPF you use, the larger the amount you must refund when you sell.

This is also why a strong paper gain and a strong cash position are not the same thing.

Two sides need to be reviewed.

First, what comes back from the sale:

Sale price, minus loan, minus CPF refund, minus costs.

Second, what is needed for the purchase:

CPF available, plus cash savings, minus the next home’s costs.

The move is only steady when both sides work together.

Can You Afford the Condo Comfortably — Not Just on Paper?

There is a difference between qualifying for a loan and feeling comfortable with it.

A bank assesses your borrowing based on income, age, existing debts, loan tenure and prevailing financing rules.

But your family still carries its own real commitments — children, parents, school fees, insurance, the unexpected.

A condo should not be planned around the maximum loan. It should be planned around a repayment that still feels manageable if life shifts.

A grounded affordability review looks beyond the price tag to the full picture: buyer’s stamp duty, ABSD if you are buying before selling, the down payment (part cash, part CPF), legal and valuation fees, renovation and furnishing, ongoing maintenance fees, property tax, moving and storage, and a cash buffer for after completion.

Moving to private usually means switching from an HDB loan to a bank loan, and bank packages get repriced over time.

So the safer question is not “What is the highest price I can buy?” It is “What price range lets us move without draining our buffer or stretching the monthly repayment?”

Should You Sell Your HDB First or Buy the Condo First?

This is one of the biggest decisions in the whole move, and the two paths carry very different risks.

Simple answer: You can buy a condo before selling your HDB, but if you still own the flat at the point of purchase, the condo may count as your second residential property. ABSD may then be payable upfront, even if you later qualify for a refund.

Should You Sell Your HDB First or Buy the Condo First?

Both sequences can work, but they carry very different cashflow, ABSD and timeline risks.

Option 1: Sell HDB First

Selling first usually gives more certainty. You know your actual sale price,

your cash proceeds and your CPF refund before you commit. In many cases,

you may also avoid paying ABSD because the flat is sold before the condo

purchase completes.

The trade-off is practical: where does the family stay before the next home

is ready? You may need an extension of stay from your buyer, a short rental,

or time with family — especially if the resale condo needs renovation or the

new launch is still being built.

Option 2: Buy Condo First

Buying first can feel reassuring because you secure the next home before

letting go of this one. But financially, it needs more care.

If you still own your HDB at the point of purchase, the condo is treated as

your second residential property. For Singapore Citizens buying a second

residential property, ABSD is currently 20% of the full purchase price.

On a $1.5 million condo, that is $300,000 — and it must be paid upfront

within the stamp duty timeline.

Important: ABSD Refund Is Pay-First, Refund-Later

For married couples, ABSD refund should not be mistaken as a waiver. In many cases, the ABSD must be paid first, then refunded later only if IRAS conditions are met.

For eligible married couples where at least one spouse is a Singapore Citizen and the property is bought jointly, the first property generally must be sold within 6 months from the purchase date of a completed second property, or within 6 months from the TOP/CSC date for an uncompleted property, whichever applies.

The refund application itself must also be made within the required timeline. Please confirm the latest rules with IRAS and your conveyancing lawyer before relying on this.

Sequence Comparison

Sell HDB first, then buy condo

Main Advantage

More certainty on proceeds and usually less ABSD pressure.

Main Risk

May need temporary accommodation before the next home is ready.

Buy condo first, then sell HDB

Main Advantage

You secure the next property earlier before letting go of your current flat.

Main Risk

ABSD may need to be paid upfront, with tighter financing and sale timeline pressure.

I once worked with an owner who had found a resale unit he loved and wanted to secure it before selling.

Once we laid out the ABSD he would need upfront, and what would happen if his HDB sale slipped past the refund window, he chose to sell first and wait three more months.

Less exciting. Far calmer.

New Launch or Resale Condo After Selling HDB?

Both can make sense. They simply suit different families.

A new launch is paid progressively, so if the project is still being built, you don’t carry the full instalment immediately — which can ease cashflow during the transition. You also get a fresh lease and new facilities.

The trade-offs: you may wait years to move in, layouts can be smaller, and you are buying off floorplans and a showflat.

A resale condo lets you see the actual unit, view, condition and neighbours, and often offers larger layouts. You can usually move sooner.

But it may need renovation, the remaining lease and maintenance condition matter, and the loan and monthly repayment tend to start sooner.

The honest question is not “new launch is better” or “resale is safer.”

It is “Which option fits our funds, timeline, family needs and future exit?”

Our new launch vs resale condo guide walks through this side by side.

Choosing the Right Condo With the Next Exit in Mind

After selling, it is tempting to focus only on what you can afford.

But affordability is one part of the decision.

The next home should also be chosen with its eventual exit in mind.

This does not mean treating every home as an investment.

It means not buying something that may be hard to sell later.

Look beyond the showflat at: entry price against nearby transactions, layout efficiency and unit size, project age and lease balance, maintenance condition and monthly fees, nearby resale competition, future supply in the area (URA planning context helps here), transport, school and family convenience, rental demand if relevant, and the future buyer pool.

A bigger unit is not always better.

A lower psf is not always a bargain.

A newer project is not always safer.

A development with strong facilities can still have weak exit demand if the entry price is stretched.

The right condo is not just the one you can enter.

It is the one you can live with comfortably and exit reasonably when the next stage comes.

Case Study: Planning Shawn’s Move From a Punggol HDB

Shawn came to me about a month before his 4-room Punggol flat reached MOP.

The first step was not to list the flat. It was to see whether the move worked on paper. We reviewed the likely sale price, the loan to redeem, the CPF refund with accrued interest, the cash that would come back, the CPF returning to his OA — and only then, what condo budget would still feel comfortable. Not the maximum. The comfortable.

What I remember most was the moment the numbers were on the table and his shoulders dropped — not because the answer was “yes,” but because he could finally see the move instead of guessing at it.

With the figures settled and the timeline mapped, Shawn and his family sold the flat and bought into a new launch, Riverfront Residences, whose progressive payment structure suited their situation.

The lesson is the part worth repeating: plan first, property-hunt second.

The move worked because it fit them — their finances, their timeline, their family, their risk comfort — before anyone signed.

This is one family’s experience in one market window. It is shared to show the planning process, not as a prediction of price performance or a result any other upgrader should expect.

Common Mistakes When Upgrading From HDB to Condo

Most mistakes don’t come from carelessness. They come from a process with many moving parts.

- Planning on paper gain. A flat may show a strong gain, but after loan redemption, CPF refund, accrued interest and costs, the cash position can look very different. Calculate real proceeds first.

- Forgetting CPF accrued interest. It is not a penalty, but it quietly reduces the cash that comes back — and it compounds over time.

- Buying first without understanding ABSD. Do not assume it is waived. For many upgraders it is paid first and refunded later only if conditions are met.

- Stretching to the maximum loan. The biggest loan is rarely the comfortable one. Leave room for rate changes, renovation and emergencies.

- Choosing by emotion only. The layout, entry price, future supply and exit demand still matter after the viewing ends.

- Ignoring the accommodation gap. Selling and buying rarely align perfectly. Plan the in-between before committing.

- Forgetting the future exit. Buy a home you can also sell reasonably when the next stage comes.

When It Is Smarter to Wait Before Upgrading

Part of good planning is knowing when not to move. A condo may suit some families; for others, the wiser answer is to wait — for now.

I would gently suggest waiting if:

- Your cash buffer would be thin after the move. If one repair, one job gap, or one rate change could create stress, the plan is too tight.

- Your income is in an uncertain season. A career switch, new business, commission swing, or an upcoming single-income period changes the comfort level fast.

- The repayment only works at today’s rate. If a modest rise makes it uncomfortable, the budget is too high.

- Your real proceeds don’t comfortably support the restructuring. If it only works by using nearly all your cash, the margin is too thin.

- The main reason is “HDB prices are high now.” A strong market is a reason to review your options — not a reason on its own to sell.

- The family is simply not ready for the transition. Timing the people matters as much as timing the numbers.

Not now does not mean never. Sometimes it means one or two years with a steadier plan. Choosing to wait is also a property decision — often a wise one.

The worst upgrades usually are not caused by bad properties. They happen when good families move before their numbers are ready.

Final Thoughts

Selling your HDB to buy a condo is more than a property transaction.

It affects your CPF, cash flow, loan commitments, and lifestyle for years to come.

So the real question is not:

“Can I upgrade?”

But:

“Will this move still feel right after the numbers settle?”

Sometimes, upgrading makes sense. Sometimes, waiting does.

The best property move is not always the biggest one — it is the one that fits your family, finances, and future plans.

If you would like to understand your sale proceeds, CPF refund, and upgrade budget before deciding, I am happy to walk through the numbers with you.

Frequently Asked Questions

Frequently Asked Questions

Common questions HDB owners ask before selling their flat and buying a condo in Singapore.

Can I sell my HDB and buy a condo?

Yes, once you meet selling eligibility, including your MOP. Before committing to the next home, check your loan, CPF refund, cash proceeds, stamp duties and affordability so the full picture is in front of you.

Should I sell my HDB before buying a condo?

Selling first usually gives more certainty, because you know your actual sale price, CPF refund and cash proceeds before you commit. The trade-off is arranging temporary accommodation or an extension if your next home is not ready.

Can I buy a condo before selling my HDB?

It can be possible, but it needs careful planning. If you still own your HDB when you buy, the condo may be treated as your second residential property, which can trigger ABSD and tighter financing.

Will I need to pay ABSD if I buy a condo before selling my HDB?

If your HDB is still under your ownership at the point of purchase, ABSD may apply because the condo counts as a second residential property. For Singapore Citizens, the current rate for a second property is 20% of the purchase price. Verify with IRAS.

Can I get ABSD back after selling my HDB?

Some married couples may qualify for an ABSD refund if IRAS conditions are met. In practice this usually means paying ABSD first and being refunded later, only if the first property is sold within the required timeline. Verify with IRAS and your conveyancing lawyer.

How long do I have to sell my HDB to get the ABSD refund?

For eligible married couples, generally within 6 months from the purchase date of a completed second property, or within 6 months from TOP/CSC for an uncompleted one. The refund application must also be made on time. Confirm with IRAS.

What happens to my CPF when I sell my HDB?

The CPF principal you used, plus accrued interest, must generally be refunded to your CPF account from the sale proceeds. If you are below 55, it usually goes to your Ordinary Account and may be reused for another home, subject to CPF rules.

Why are my cash proceeds lower than my profit?

Because paper gain does not account for loan redemption, CPF refund, accrued interest and selling costs. Your actual cash to bank is only known after those amounts are deducted.

How much cash do I need to upgrade from HDB to condo?

It depends on your proceeds, CPF refund, available CPF, the next price, loan amount, stamp duties, renovation and buffer. The safest approach is to calculate both sides — what comes back, and what the purchase requires.

What if my sale proceeds are not enough?

Then it may be better to reduce the condo budget, wait longer, build more savings, or look at a different option. Upgrading should not depend on stretching every dollar.

New launch or resale condo after selling HDB?

It depends on your timeline and needs. A new launch suits families who can wait and prefer progressive payments; a resale suits those who need to move sooner and want to see the actual unit. Either way, consider future exit demand.

Is upgrading to a condo worth it in Singapore?

It can be, when the move fits your finances, family needs, timeline and long-term plan. It may not be if it creates repayment stress, drains your buffer, or depends on optimistic appreciation assumptions.

Will it get harder to upgrade from HDB to a condo in future?

The gap between HDB and private prices has widened over the past decade, which makes some owners want to move earlier. But a past trend is not a forecast, and recent supply changes make the future uncertain. Decide on your own numbers, not the trend.

When should I not upgrade from HDB to condo?

Consider waiting if your cash buffer is thin, your income is uncertain, the repayment only works at today's rate, your real proceeds don't comfortably support the move, or the main driver is market excitement rather than family need.

What are the most common mistakes HDB upgraders make?

Planning on paper gain, ignoring CPF accrued interest, buying before selling without understanding ABSD, stretching to the maximum loan, overlooking temporary accommodation, and choosing a condo without thinking about future exit.

What My Clients Say | Genuine Experiences

Real stories, real experiences—because your journey deserves nothing less than the best.

Awards and Accolades

Self Introduction

Hi, I’m Rick Long,

Associate Senior Division Director, Huttons Asia · CEA Reg. R026818Z

With decades of experience in Singapore’s real estate market, I’ve had the privilege of being mentioned in media outlets such as Channel NewsAsia, The Straits Times, and 99.co.

Over the years, I’ve written extensively on the local property landscape — tackling the real questions buyers and sellers face, and helping them navigate each step with greater steadiness and confidence.

Many of my clients have become long-time friends — their trust and kind reviews continue to inspire me to raise the bar in everything I do.

I believe real estate should be strategic, seamless, and deeply aligned with your life’s journey.

Related Articles:

Ever wonder if you are suitable for Sell one buy two investment concept? – Read more (Sell one buy two)

Is buying new launch or resale condo have better returns? – Read more (New Launch vs Resale condo)

Looking to upgrade from Hdb to condo? – Read more (Sell Hdb buy condo)

What to take note when selling Hdb resale flat? – Read more (Hdb Resale Process)

Buying another Hdb flat, and using the fund from current home? – Read more (Hdb contra)

Why do some Hdb flat price depreciate so much? – Read more (Hdb depreciation curve)

What is one of the most common reason for property negative sales? – Read more (Cpf accrued interest)

Financial calculation for selling a Hdb flat? – Read more (Hdb resale calculator)

Buying EC before selling your HDB? – Read more (Upgrade to EC before selling your HDB)

Should you sell your EC after 5 years? – Read more (Selling EC)