HDB Resale Process in Singapore: Step-by-Step Guide for Sellers

Selling your HDB flat is not just about finding a buyer.

It is a sequence of decisions — checking your sale proceeds, understanding your CPF refund, registering your Intent to Sell, preparing your unit for marketing, assessing buyer readiness, handling the OTP, submitting the resale application, and planning the handover.

Each step is manageable.

But when sellers rush into the process without understanding the numbers or timeline, small gaps can become stressful later — especially if they are also planning to buy another home after selling.

That is why the HDB resale process should not be treated as a simple checklist.

It should be treated as a planned transition.

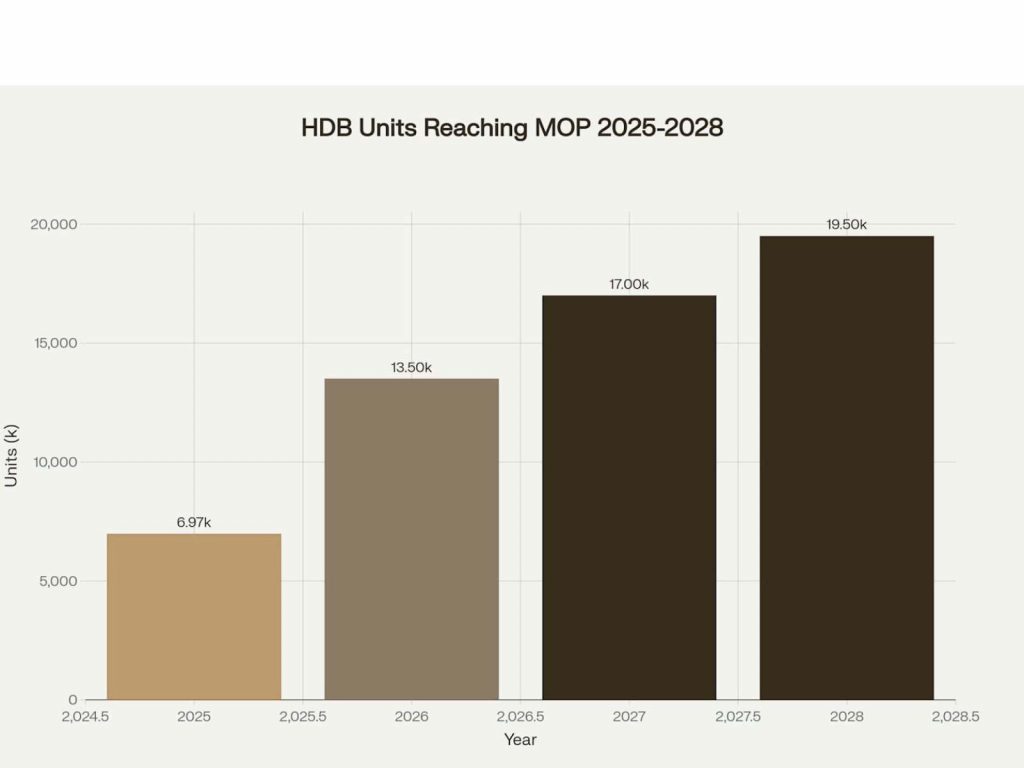

In 2026, this matters even more. More flats are expected to reach MOP compared with 2025, and buyers are generally more data-aware when comparing recent transactions, asking prices, remaining lease and financing limits.

That does not mean every seller will struggle.

It simply means preparation, pricing and timeline planning matter more than before.

This guide walks you through the HDB resale process step by step, so you know what to expect before you commit.

Table of Contents

Quick Answer: How the HDB Resale Process Works

At a high level, selling an HDB flat in Singapore usually involves three broad stages.

Stage 1 — Preparation

Before listing the flat, you should work out your real sale proceeds, check your CPF refund amount, understand your outstanding loan, and register your Intent to Sell on the HDB Flat Portal.

Stage 2 — Marketing and buyer commitment

You prepare your pricing and marketing, host viewings, negotiate with buyers, and grant the Option to Purchase once the buyer is ready and the terms are acceptable.

Stage 3 — HDB resale application and completion

After the buyer exercises the OTP, both parties submit the resale application through the HDB Flat Portal. HDB then processes the application, arranges the necessary checks, requires both parties to endorse the resale documents, and eventually completes the transaction.

For many sellers, the full process can take several months from preparation to completion. The exact timeline depends on your pricing, buyer response, documentation, HDB processing, buyer financing, and whether you are also buying another home.

Before You Start: Calculate Your Real Sale Proceeds

This is the step many sellers underestimate.

The price you sell for is not the amount you receive in cash.

Your actual cash proceeds depend on several moving parts:

Your selling price

Your outstanding housing loan

Your CPF refund amount

CPF accrued interest

Legal, admin and selling-related costs

Any agent commission, if applicable

A simple way to think about it:

Estimated Cash Proceeds = Sale Price − Outstanding Loan − CPF Refund − Selling Costs

Your CPF refund includes the CPF principal used for the flat plus the accrued interest. CPF explains that if CPF savings were used for a property, the principal amount withdrawn and accrued interest must be refunded when the property is sold.

This money is not “lost”. It goes back into your CPF account.

But it can affect how much cash you have available after the sale, especially if you are planning to use the proceeds for your next home.

In real consultations, this is often where the conversation changes.

A seller may start with the question:

But after checking the CPF refund, loan balance and next-home budget, the better question becomes:

“After I sell, does the next move still make sense?”

That is why the real calculation should happen before marketing — not after receiving an offer.

Where to check your numbers

You should verify your CPF refund directly through CPF, check your outstanding loan with HDB or your bank, and include estimated selling costs before making any decision.

CPF states that property sale refunds are processed within 15 working days after CPF receives the funds.

Before you list, it is worth knowing what you may actually walk away with after CPF refund, outstanding loan and selling costs.

Register Intent to Sell

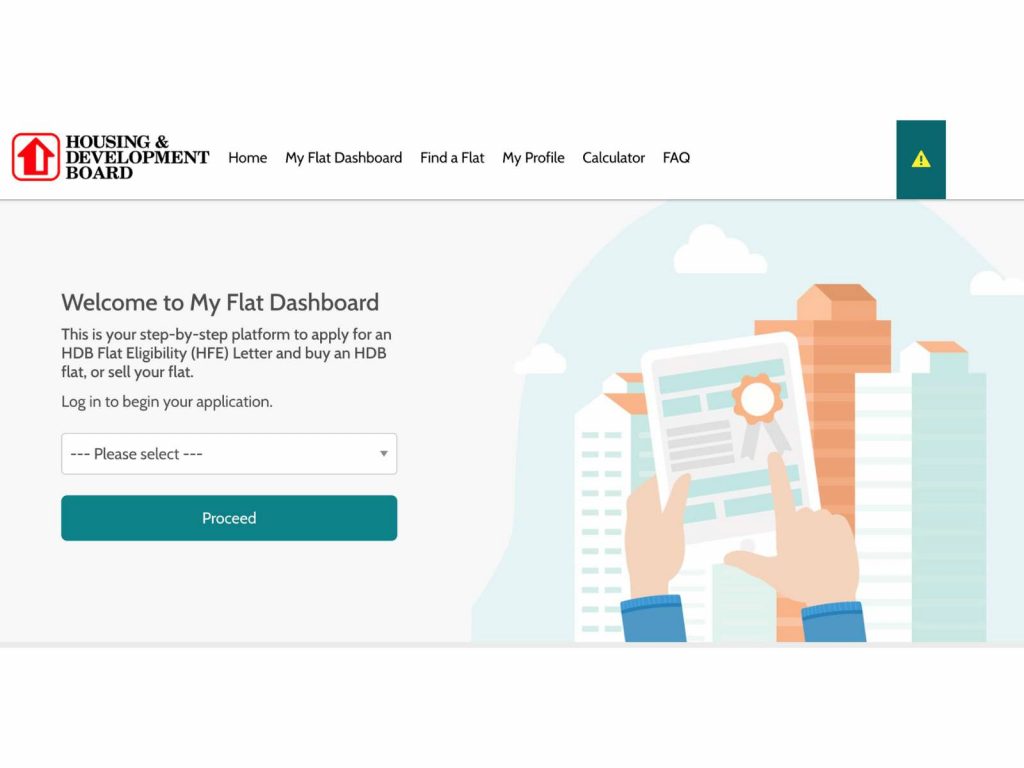

Before granting an Option to Purchase, you must register your Intent to Sell through the HDB Flat Portal.

HDB states that the Intent to Sell is valid for 12 months, and it must be valid when you grant the OTP and when you submit the resale application.

You must also register Intent to Sell for at least 7 days before you may grant an OTP to flat buyers.

This is why it is usually better to register early once you are seriously considering a sale.

The 7-day period can run in the background while you prepare your pricing, marketing and documents. If you wait until a serious buyer appears, you may create unnecessary delay.

What this step helps you check

Registering your Intent to Sell helps confirm important eligibility points, including whether you have met the Minimum Occupation Period and whether there are any selling conditions that may affect the transaction.

For sellers, this is not just an admin step.

It is the formal starting point before you can issue an HDB OTP.

Check Buyer Readiness Before Granting OTP

Before granting the Option to Purchase, do not look only at the offered price.

You should also check whether the buyer is ready to proceed.

A high offer is not useful if the buyer’s financing, eligibility or timeline is not properly prepared.

For HDB resale buyers, the HFE letter is an important part of buyer readiness.

HDB states that buyers must have a valid HFE letter before they obtain an OTP from a flat seller.

The HFE letter helps buyers understand their eligibility, housing grants and HDB loan amount, where applicable.

Before granting OTP, it is reasonable to check:

Whether the buyer has a valid HFE letter

Whether the buyer’s financing is prepared

Whether all co-buyers are aligned

Whether the buyer’s timeline matches your own plans

Whether the agreed price may create valuation or cash-over-valuation concerns

This matters because once you grant the OTP, your flat is effectively tied to that buyer during the option period. If the buyer is not properly ready, you may lose time and momentum.

How the 75% LTV change affects sellers

From 20 August 2024, the Loan-to-Value limit for HDB housing loans was lowered from 80% to 75%.

For sellers, this does not mean every buyer will have difficulty.

But some buyers may become more price-sensitive, especially if their financing is close to the limit.

That is why seller preparation is no longer just about presenting the flat well.

It is also about understanding whether the buyer in front of you can realistically complete the purchase.

The 12-Step HDB Resale Process

Once you understand your numbers and have registered your Intent to Sell, the actual resale process becomes easier to follow.

The steps below show what usually happens from preparation to completion.

Step 1 — Work Out Your Real Sale Proceeds

Estimated timeline: 1 to 2 days

Before marketing your flat, start with the numbers.

You should check:

Estimated selling price

Outstanding housing loan

CPF refund amount

CPF accrued interest

Legal, admin and selling-related costs

Expected cash proceeds after completion

This step matters because your selling price is not your final cash amount.

A flat may sell at a strong price, but if the CPF refund and loan balance are high, the actual cash proceeds may be lower than expected.

This should be checked before you set your asking price, before you make plans for your next property, and definitely before you accept an offer.

Step 2 — Decide Whether to DIY or Engage Help

Estimated timeline: Before marketing starts

Some sellers prefer to handle the sale themselves. Others prefer to engage an agent to manage pricing, marketing, viewings, negotiation, paperwork and timeline planning.

There is no single right answer.

DIY may work if your case is straightforward, your timeline is flexible, and you are comfortable managing the process directly.

Professional help becomes more useful when there are more moving parts, such as:

Selling and buying around the same period

CPF and cash-flow planning

Buyer financing concerns

Valuation risk

Multiple owners involved

Tight completion timeline

The key is to choose the route that matches the complexity of your sale, not just the route that looks cheaper at the start.

Step 3 — Register Your Intent to Sell

Estimated timeline: About 15 minutes online, followed by HDB’s required 7-day cooling-off period

You must register your Intent to Sell through the HDB Flat Portal before you can grant an Option to Purchase.

After registration, HDB requires a 7-day cooling-off period before you may grant the OTP.

This is meant to give sellers time to think through the sale, plan their next housing arrangement and avoid committing too quickly.

Do not leave this to the last minute.

Once your Intent to Sell is registered, the 7-day cooling-off period can run in the background while you prepare your pricing, marketing, documents and viewing schedule.

Step 4 — Prepare Your Pricing and Marketing

Estimated timeline: 1 to 2 weeks

This is where many sellers either create strong buyer interest or weaken their own position.

Good marketing is not just about making the flat look nice.

It is about helping buyers understand the value of the home quickly and confidently.

A proper marketing setup should include:

Clean and well-lit photos

Accurate floor plan

Recent transaction references

Clear explanation of flat condition

Key selling points such as floor level, layout, amenities, transport and remaining lease

Realistic pricing based on current market evidence

Avoid pricing only from the highest nearby transaction.

That transaction may have a different floor level, condition, view, layout, remaining lease, ethnic quota situation, buyer urgency or negotiation context.

A strong asking price should still be defendable.

Step 5 — Conduct Viewings Professionally

Estimated timeline: Ongoing during marketing period

Viewings are where buyers test whether the listing matches reality.

Before each viewing, make sure the flat is clean, bright, ventilated and easy to walk through.

During the viewing, buyers usually want to assess:

Space and layout

Natural light

Noise level

Condition of the flat

Privacy

Storage

Neighbourhood convenience

Renovation or repair concerns

Whether the home feels suitable for their family

A calm viewing works better than a hard sell.

Give buyers enough information, then give them space to discuss. Serious buyers often need a second viewing before making a firm offer, so follow-up speed matters.

Step 6 — Negotiate and Grant the Option to Purchase

Before granting the OTP, check three things carefully:

Intent to Sell — Has your Intent to Sell been registered, and has the 7-day cooling-off period passed?

Buyer readiness — Does the buyer have the required HFE letter and financing preparation?

Price and timeline — Are the offer and completion timeline acceptable for your next step?

Once the OTP is granted, your flat is tied to that buyer during the option period.

You cannot simply issue another OTP to a different buyer during that time.

This is why sellers should not grant OTP based on price alone.

A high offer from an unprepared buyer may create more stress than a slightly lower offer from a buyer who is ready, properly financed and aligned on timeline.

Step 7 — Buyer Requests HDB Valuation

Estimated timeline: Usually after OTP is granted

After the OTP is granted, the buyer may request an official HDB valuation if they are using CPF savings or a housing loan.

This valuation affects how much CPF and loan the buyer can use.

If the valuation is lower than the agreed sale price, the difference is known as Cash Over Valuation, or COV.

For the buyer, COV must be paid in cash.

For the seller, this is where valuation risk appears.

If the COV is higher than the buyer expected, the buyer may become hesitant, request a discussion, or allow the OTP to lapse if they are not comfortable proceeding.

This is why pricing should be ambitious but still grounded in recent evidence.

Step 8 — Buyer Exercises the OTP

Estimated timeline: Within 21 calendar days from OTP grant

If the buyer decides to proceed, they will exercise the OTP within the option period.

At this point, the buyer pays the exercise fee.

The option fee and exercise fee combined cannot exceed $5,000.

Once the OTP is exercised, both seller and buyer are committed to the transaction.

This is the point where sellers should begin preparing more seriously for:

Resale application submission

Required documents

Moving timeline

Next accommodation or next purchase planning

Completion arrangements

Before reaching this point, make sure you are comfortable with the agreed price, timeline and buyer profile.

Step 9 — Submit the Resale Application

Estimated timeline: After OTP is exercised

After the OTP is exercised, both seller and buyer submit their respective portions of the resale application through the HDB Flat Portal.

This is an important administrative stage.

The second party must submit their portion within the required timeframe after the first party submits.

If the submission window is missed, the application may lapse and the parties may need to submit again.

Sellers should prepare the necessary documents early, especially if there are special circumstances such as:

Marriage or divorce matters

Deceased co-owner

Power of Attorney

Multiple owners

Contra or sell-buy planning

Any documentation that may require more time to retrieve

The smoother your documents, the smoother this stage tends to be.

Estimated timeline: During HDB processing period

HDB will inspect the flat as part of the resale process.

The inspection is not about whether your home looks newly renovated.

It is mainly to check that the flat does not have unauthorised works or issues that may affect safety or compliance.

Common areas of concern include:

Walls removed or altered without approval

Unauthorised structural changes

Unapproved window or grille works

Plumbing or electrical changes

Leaks, water damage or visible defects

Renovation works without proper records

If you suspect there may be an issue, address it early.

The worst time to discover a renovation compliance problem is after the buyer has exercised the OTP and everyone is waiting for completion.

Step 11 — Endorse the Resale Documents

Estimated timeline: After HDB prepares the resale documents

When the resale documents are ready, HDB will notify both parties to endorse them through the HDB Flat Portal.

This stage should be taken seriously.

The documents may include payment details, declarations, undertakings and completion arrangements.

Before endorsing, sellers should check:

Sale price

Completion date

Names of all parties

Payment breakdown

CPF refund information

Any undertakings or special conditions

Do not rush through this stage just because it feels administrative.

Once documents are endorsed, changes may be difficult or may delay the transaction.

Step 12 — Completion and Key Handover

Estimated timeline: Usually after HDB completes the required processing and approval steps

At completion, the legal transfer of the flat is finalised.

Sellers should prepare:

All keys

Letterbox keys

Manuals or remote controls, where applicable

Utility and town council arrangements

Final move-out

CPF refunds are handled after completion.

To be safe, we will phrase it this way:

CPF refunds are processed within 15 working days after CPF receives the funds.

This is important if you are relying on the returned CPF funds or cash proceeds for your next move.

Build in enough buffer, especially if you are selling and buying within a tight timeline.

How to Plan Your Selling Timeline Properly

Knowing the HDB resale steps is one thing.

Planning the timeline around your actual life is another.

For most sellers, the real question is not only “How long does the resale process take?”

The more useful question is: “When do I need to move, when do I need the funds, and what must happen before I commit to the next step?”

This matters especially if you are selling your current HDB flat and planning to buy another home after that.

Not sure whether to sell first or buy first?

Answer 5 quick questions to see which sequence may need closer planning before you commit. This is a guide, not a financial recommendation.

This tool is meant to help you think through the sequence. It does not replace a proper review of your CPF refund, loan eligibility, sale proceeds and next-home financing.

Common Mistakes Sellers Should Avoid

Most HDB resale problems do not happen because the process is impossible.

They happen because one step was assumed too early.

Here are the common mistakes sellers should avoid.

Common HDB Selling Mistakes Sellers Should Avoid

Most HDB resale problems do not happen because the process is impossible. They happen because one step was assumed too early. Here are the common mistakes worth checking before you list.

Some sellers start marketing based on an estimated selling price, then only check their CPF refund and loan balance later.

That can be risky because your sale price is not your take-home cash. CPF refund, accrued interest, outstanding loan and selling costs can change the final amount significantly.

If you are planning to buy after selling, this number affects your next budget.

After registering your Intent to Sell, HDB requires a 7-day cooling-off period before you can grant an OTP to a buyer.

This is not a flexible waiting period. If you register only after a serious buyer appears, you may not be able to issue the OTP immediately.

That delay can affect momentum, especially if the buyer is comparing other flats.

Not always. A high offer is attractive, but price is only one part of the decision.

Before granting OTP, you should also check whether the buyer is financially and administratively ready. This includes their HFE letter, financing preparation, co-buyer alignment, timeline, and possible valuation or COV concerns.

The highest nearby transaction is useful, but it may not be the right benchmark.

That flat may have had a better floor level, renovation, facing, remaining lease, buyer urgency, ethnic quota situation, or less competing supply at the time.

For HDB resale buyers using CPF or a housing loan, valuation affects how much CPF and loan they can use.

If the agreed price is above HDB’s valuation, the difference becomes Cash Over Valuation, which the buyer must pay in cash.

This does not mean sellers should avoid strong pricing. But the asking price should be supported by recent evidence so the buyer understands the risk before committing.

After the buyer exercises the OTP, both seller and buyer must submit their respective portions of the resale application.

The second party must submit within 7 calendar days after the first party submits. HDB also gives parties 6 calendar days to endorse resale documents once they are ready.

Missing these windows can cause unnecessary delay.

HDB inspection can surface unauthorised renovation works, altered walls, leaks, or other compliance concerns.

If these appear late in the process, they can delay completion or create stress with the buyer.

The sale is only one side of the move.

You still need to plan when you will move out, whether you need temporary accommodation, whether to sell first or buy first, and how CPF refund timing affects your next purchase.

CPF refunds are processed within 15 working days after CPF receives the funds.

Before you list, make sure the sale is planned in the right order.

A good offer can still become stressful if the numbers, procedure and timeline are not properly mapped first.

DIY vs Engaging an Agent

Some HDB sellers are comfortable managing the process themselves.

Others prefer to have someone handle the pricing, marketing, viewings, buyer screening, negotiation, paperwork and timeline coordination.

There is no single right answer.

The better question is:

How straightforward is your sale?

DIY may work if your situation is simple

Selling on your own may be suitable if:

Your flat has no renovation or compliance concerns

You have already checked your CPF refund and loan balance

You are comfortable handling buyer enquiries and viewings

You understand the HDB resale process and key timelines

You are confident negotiating directly with buyers

You are not rushing to sell and buy another home at the same time

Your co-owners are aligned on the price, timeline and next step

For sellers with time, patience and a straightforward case, DIY can be a workable route.

But it still requires attention to detail.

You are not only marketing the flat.

You are also managing buyer readiness, OTP timing, resale application submission, HDB endorsement, completion arrangements and handover.

Professional help may be useful when there are more moving parts

An agent may be more helpful when the sale is not so straightforward.

For example:

You are selling and buying around the same time

You need the sale proceeds or CPF refund for your next purchase

You are unsure how to price the flat against recent transactions

You need stronger marketing, photos, copywriting or buyer reach

You are dealing with buyer financing, HFE or valuation concerns

You have past renovation works that may need checking

There are multiple owners or family members involved

Your timeline is tight

You prefer to have someone manage the process and negotiations

In these cases, the value of help is not only in “finding a buyer”.

It is in reducing mistakes, protecting the timeline, managing expectations and helping the seller make decisions with a more complete picture.

The right way to think about this is not simply:

“Can I save the commission?”

A better set of questions would be:

“Can I manage the process properly myself?”

“Can I negotiate as confidently as a professional who handles this every week?”

“Can I achieve the same final sale price — or better?”

For example, if selling on your own helps you save $15,000 in commission, that sounds meaningful.

But if a stronger pricing strategy, marketing presentation, buyer reach and negotiation process helps the flat sell for $25,000 more, the overall difference may still be a $10,000 net gain after accounting for the commission.

Of course, this is not guaranteed.

The point is not that an agent will always sell higher.

The point is that the real comparison should be based on the overall outcome, not just the visible commission cost.

For some sellers, DIY may still make sense.

For others, the value of professional help may come from stronger positioning, better negotiation, fewer mistakes, smoother timelines and a more controlled process.

The choice should match your situation — not just the desire to save costs.

HDB Resale Process FAQ

Common Questions About the HDB Resale Process

Use this FAQ to quickly understand the key timing, CPF, OTP, valuation and sell-buy questions sellers usually ask before listing their HDB flat.

For many sellers, the full process can take a few months from preparation to completion.

The timeline depends on how long marketing takes, how quickly a suitable buyer is found, whether the buyer exercises the OTP, how smoothly both parties submit the resale application, and when HDB accepts and completes the transaction.

You should register your Intent to Sell once you are seriously preparing to sell.

This is because HDB requires a 7-day cooling-off period after registration before you can grant an OTP.

No.

After registering your Intent to Sell, you must wait out HDB’s 7-day cooling-off period before granting an OTP.

Yes. For HDB resale buyers, the HFE letter is an important part of buyer readiness.

Before granting OTP, sellers should check that the buyer has the required HFE letter and has thought through financing.

After you grant the OTP, the buyer has up to 21 calendar days to decide whether to exercise it.

During this time, the buyer may request an HDB valuation if they are using CPF savings or a housing loan.

If the buyer exercises the OTP, both parties move toward submitting the resale application.

If the agreed sale price is higher than HDB’s valuation, the difference is known as Cash Over Valuation, or COV.

The buyer must pay this difference in cash.

For sellers, this is why it is important to price the flat based on recent comparable transactions, not only the highest number in the area.

Your sale proceeds are settled around completion, after deducting items such as the outstanding loan, CPF refund and selling-related costs.

CPF refunds are processed within 15 working days after CPF receives the funds.

If you used CPF savings for the flat, you generally need to refund the CPF principal used plus accrued interest back to your CPF account when the property is sold.

This is not money lost. It goes back into your CPF.

Yes, many sellers choose to sell first because it gives them a clearer picture of their actual proceeds before committing to the next purchase.

The trade-off is that you may need temporary accommodation or a transition plan before moving into your next home.

It may be possible, depending on your finances and the type of property you are buying.

But buying first can create more financial pressure if you need the sale proceeds from your current flat, or if your sale takes longer than expected.

If HDB identifies unauthorised works or compliance issues, you may need to rectify them before completion.

This can delay the transaction and create stress for both seller and buyer.

Usually, major renovation before selling is not necessary.

Most sellers are better off focusing on cleaning, decluttering, minor repairs, lighting, paint touch-ups and proper presentation.

Buyers often prefer to renovate based on their own taste.

Still unsure how your sale should be planned?

Before you list, it is worth getting a professional view on your likely sale proceeds, timeline and next-step options.

Conclusion

Selling your HDB flat is a process that rewards preparation.

The smoother sellers are usually not the ones who simply “try their luck” with a high asking price.

They are the ones who understand their numbers early, register their Intent to Sell on time, check buyer readiness before granting OTP, prepare the right documents, and plan the timeline around what comes after the sale.

Before you list your HDB flat, make sure the sale is planned in the right order.

A good offer can still become stressful if the numbers, procedure and timeline are not planned properly.

TLDR

What My Clients Say | Genuine Experiences

Real stories, real experiences—because your journey deserves nothing less than the best.

Awards and Accolades

Self Introduction

Hi, I’m Rick Long,

Associate Senior Division Director, Huttons Asia · CEA Reg. R026818Z

With decades of experience in Singapore’s real estate market, I’ve had the privilege of being mentioned in media outlets such as Channel NewsAsia, The Straits Times, and 99.co.

Over the years, I’ve written extensively on the local property landscape — tackling the real questions buyers and sellers face, and helping them navigate each step with greater steadiness and confidence.

Many of my clients have become long-time friends — their trust and kind reviews continue to inspire me to raise the bar in everything I do.

I believe real estate should be strategic, seamless, and deeply aligned with your life’s journey.

Related Articles:

Ever wonder if you are suitable for Sell one buy two investment concept? – Read more (Sell one buy two)

Is buying new launch or resale condo have better returns? – Read more (New Launch vs Resale condo)

Looking to upgrade from Hdb to condo? – Read more (Sell Hdb buy condo)

What to take note when selling Hdb resale flat? – Read more (Hdb Resale Process)

Buying another Hdb flat, and using the fund from current home? – Read more (Hdb contra)

Why do some Hdb flat price depreciate so much? – Read more (Hdb depreciation curve)

What is one of the most common reason for property negative sales? – Read more (Cpf accrued interest)

Financial calculation for selling a Hdb flat? – Read more (Hdb resale calculator)

Buying EC before selling your HDB? – Read more (Upgrade to EC before selling your HDB)

Should you sell your EC after 5 years? – Read more (Selling EC)