Should You Sell Your HDB Flat? How to Decide Whether to Sell or Wait

Sell your HDB when the move gives you more room, not less.

Check four things first: whether your next home is financially workable, what your proceeds are after loan redemption and CPF refund with accrued interest, whether waiting would genuinely improve your position, and whether the timing is driven by planning rather than pressure.

Most HDB owners are not asking whether they can sell.

They are asking whether selling now will actually work better for what comes next.

A strong sale price on its own does not answer that.

What decides it is what you keep after the loan and the CPF refund, what the next move costs, and whether the move leaves you with more options or fewer.

For some owners the numbers already work and waiting adds little.

For others the next purchase is not yet settled, the proceeds have not been worked out, or the move is being driven more by pressure than by planning.

This guide is built around the position you would actually be in after the move — starting with what the market data currently shows.

Already decided to sell and looking for the steps?

The HDB resale process guide covers the procedure from Intent to Sell through to completion.

Quick Answer: Should You Sell Your HDB Now or Wait?

If your next move is already workable, your flat is facing growing competition, and waiting is unlikely to improve your position, selling now may make sense.

If your next purchase plan is not yet settled, your take-home proceeds have not been worked out, or the move is being driven by stress rather than structure, waiting may be the better move.

There is no one-size-fits-all answer. Sell when the move gives you more room, not less — and wait only when the delay has a real purpose behind it.

HDB Seller Decision Tool

Should You Sell Your HDB Now or Wait?

A quick direction-check based on one principle: sell when the move gives you more room, not less.

This needs a closer look.

This is the starting position. Adjust the six questions above to see a direction based on your own situation.

What your answers suggest

Watch-outs

This is a direction check, not financial advice. It does not replace a proper review of your CPF refund, outstanding loan, likely sale proceeds and next-home financing.

The factors, side by side

Six things decide this, and each one can point either way depending on your situation. Read down the rows and see where you actually sit.

| Factor | Points toward selling now | Points toward waiting |

|---|---|---|

| Your next move | You know what you are buying next, and it is costed. | The next purchase is not yet settled, or the budget is still a rough idea. |

| Your take-home proceeds | Worked out properly — loan redemption, CPF refund and accrued interest all known. | Still an estimate, so the cash position is not real yet. |

| What waiting would change | Nothing you can name specifically. Waiting is a pause, not a plan. | Something specific: savings, loan readiness, a school year, a family timeline. |

| Your timeline | Enough room to sell, complete and transition without pressure. | A fixed date you cannot move, with no plan yet for the gap between homes. |

| Your flat's market position | More comparable flats are reaching MOP in your town, and your buyer pool has widened — since 28 July 2026, private property owners and former owners can buy a non-subsidised resale flat with no waiting period, which matters most for larger flats. | Your flat has attributes that stay scarce whatever the supply — floor, layout, location, remaining lease or condition. |

| What is driving the decision | Planning and readiness. The move serves a real need. | A headline, a neighbour's sale, or a worry about missing out. |

How to use this. Do not total it up. Most owners find themselves on both sides, and that is normal — it means the decision turns on which rows carry the most weight for them, not on a score.

In practice, two rows do most of the work: your take-home proceeds and your next move. When those two point the same way, the rest usually follows. When they disagree, that disagreement is the real question — and it is worth resolving before you list.

Supply and demand move differently by town, so the market-position row is the one most worth checking against your own estate. The HDB Downgrader Watch tracks demand, rental and cash-over-valuation by town and is updated as new data is released.

Table of Contents

Is Now a Good Time to Sell an HDB Flat?

What the numbers say for HDB sellers right now

Three things shape a seller's position: where prices have moved, whether buyers are still active, and how many flats are coming to market alongside yours. Here is each, from official figures.

| Period | Change |

|---|---|

| 2022 (full year) | +10.4% |

| 2025 (full year) | +2.9% |

| 1Q 2026 | −0.1% |

| 2Q 2026 | −0.3% |

| 1H 2026 (cumulative) | −0.4% |

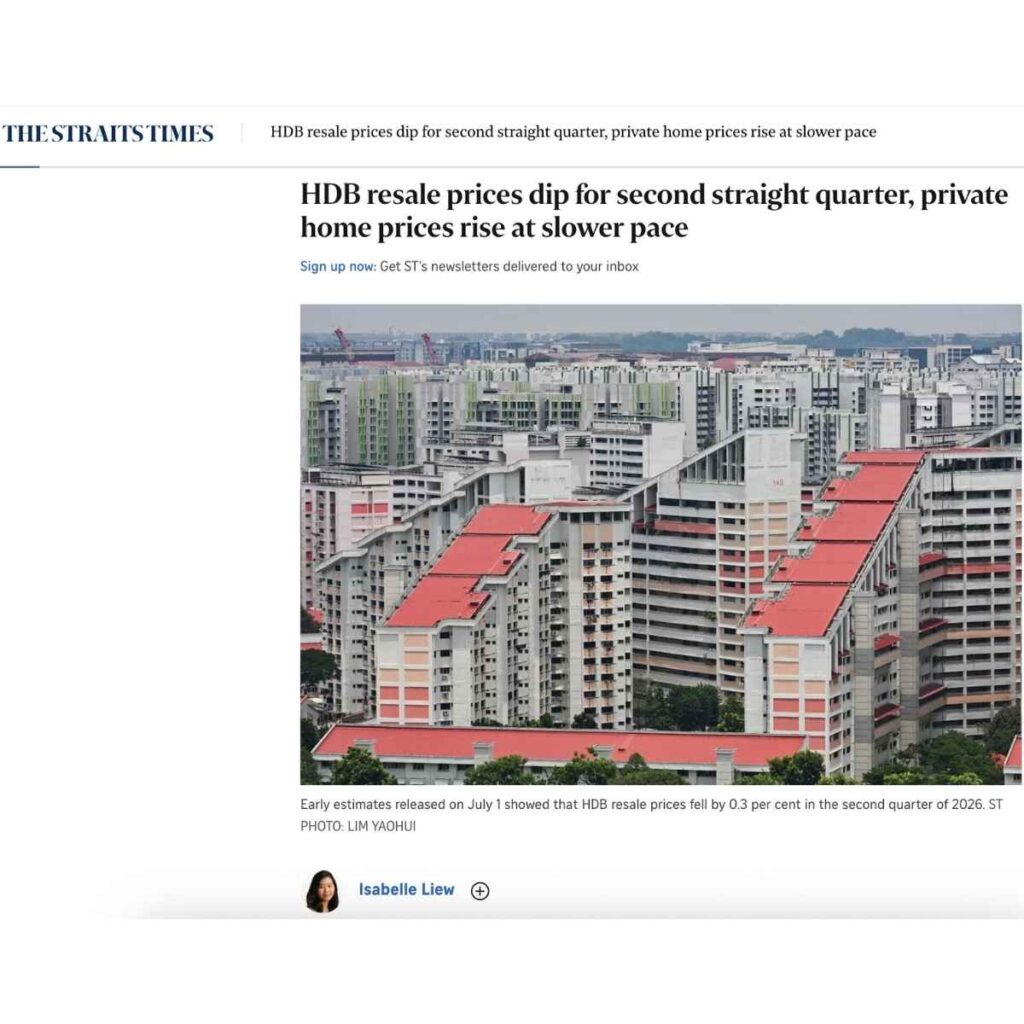

The index stood at 202.8 at the end of 2Q 2026 (base: 1Q 2009 = 100). The 1Q and 2Q falls are the first back-to-back quarterly declines since 2019.

| Measure | 1Q 2026 | 2Q 2026 | Change |

|---|---|---|---|

| Resale transactions | 6,285 | 6,396 | +1.8% |

| Approved rental applications | 9,535 | 10,002 | +4.9% |

Resale volume rose over the quarter, but sat roughly 10% below the same quarter a year earlier.

| Year | Flats reaching MOP |

|---|---|

| 2025 | about 8,000 |

| 2026 | about 13,500 |

| 2027 | about 15,000 |

| 2028 | about 19,500 |

A flat reaching MOP becomes eligible to be sold. Not every eligible flat is listed, so these figures show the size of the pool, not the number of listings.

How to read this as a seller. Two things are true at once. Prices have eased slightly over two quarters, while buyers have stayed active — so softer prices have not meant a stalled market.

The pipeline is the part that touches you directly. More flats becoming eligible to sell means more choice for buyers, and more homes competing for attention alongside yours. Whether that affects your flat depends on your town, flat type, floor, remaining lease and condition — the market has not moved evenly.

None of this predicts where prices go next. It describes the position you would be selling into today.

Sources: Housing & Development Board resale price index and quarterly resale and rental statistics, 2Q 2026 release (24 July 2026); Ministry of National Development and HDB joint statement on the removal of the 15-month wait-out period (28 July 2026). Figures as at 1 August 2026. MOP figures are the ministries' stated estimates and are rounded. Verify the latest figures at hdb.gov.sg before relying on this table.

The HDB resale price index has now fallen for two consecutive quarters — down 0.1% in the first quarter of 2026, and a further 0.3% in the second, to 202.8.

That is the first back-to-back decline in nearly seven years, and it leaves the index around 0.4% lower across the first half of the year.

Demand has not disappeared. Resale volume rose 1.8% over the quarter, from 6,285 transactions to 6,396 — though that is roughly 10% below the same quarter a year earlier. Prices softened while buyers stayed active.

Supply is the part worth watching. MND and HDB have said around 13,500 flats reach their minimum occupation period in 2026, rising to about 15,000 in 2027 and 19,500 in 2028.

None of that tells you what your own flat will do. Some flats still draw strong interest on location, condition or scarcity; others meet more resistance where buyers have more to choose from.

What the figures do say is that waiting no longer carries an automatic assumption of a better position later — and that the number of flats coming to market alongside yours is rising.

One change also works in your favour as a seller.

Since 28 July 2026, private property owners and former owners can buy a non-subsidised resale flat immediately, without the previous 15-month wait — which widens the pool of buyers your flat sells into, particularly for larger flats.

If the property you are timing is a private home or an investment unit rather than an HDB flat, that decision runs on different rules, including the Seller’s Stamp Duty holding period.

The Real First Question to Ask Before Selling Your HDB Flat

5 Numbers to Check Before You Decide

This gives you a starting point, not a conclusion. The key is not just what price sounds possible, but what price is realistic in the current market for your flat’s location, condition, floor level, remaining lease, and competition.

This amount has to be cleared first. A seller who overlooks this may overestimate how much flexibility they will have after the sale.

If CPF was used for the home, it has to be refunded back into CPF upon sale, subject to the actual sale proceeds and prevailing rules. This is one of the biggest reasons homeowners are surprised by how much less cash they walk away with.

This is where the picture becomes real. After accounting for your loan, CPF refund obligations, and sale-related costs, what is actually left for your next move?

This includes more than just the next purchase price. You may also need to think about downpayment, stamp duties, renovation, temporary housing, and whether the monthly holding cost still feels safe.

Example: A sale that looks strong, but feels different after the breakdown

- Sale Price: $900,000

- CPF Refund (Principal + Accrued Interest): -$250,000

- Outstanding Loan: -$300,000

- Miscellaneous Costs: -$20,000

It becomes about possibility.

Factors That Point Toward Selling Now

- you are upgrading for space or lifestyle fit

- you are rightsizing to reduce load or free up flexibility

- you want to move closer to schools, work, or family

- you want to reposition into a home that better suits the next phase of life

When the Next Move Is Also About Long-Term Upside

And it does not mean upgrading is automatically the right financial move.

About these transaction figures. These are selected examples, chosen because they recorded a gain. They are not a representative sample and should not be read as typical. Across any set of private property transactions over a comparable period, outcomes vary widely — some flat, some negative.

The amounts shown are gross differences between purchase and sale price. They are before CPF refund and accrued interest, outstanding loan redemption, stamp duties, agent commission, legal fees and holding costs, so the cash actually received in each case was lower — in some cases materially so.

Past transactions are not an indication of future results. Nothing here is a forecast, a projection, or a promise about any other property, including yours. Verify any figure independently before relying on it.

Factors That Point Toward Waiting

The CPF Refund Trap Most HDB Sellers Miss

The CPF Refund Trap, Simplified

When you sell, the CPF you used for the property — plus accrued interest — generally needs to be refunded to your CPF account first.

Want to see your actual CPF refund and likely cash in hand based on your own numbers?

Request a seller reviewThese figures are illustrative and opinion-based, produced with calculation tools — not a valuation or financial advice. Human error is possible; verify against official sources before relying on them.

Sale Price Is Not Your Real Take-Home

How much profit will I make?

Did someone else in the block sell higher?

- your outstanding housing loan

- your CPF used plus accrued interest

- legal fees and sale-related expenses

- any agent fees

- the practical cost of your next move, including renovation, temporary housing, or other transition costs

Understanding Your Property Sale

A strong sale price can look exciting. But what matters next is how much you may actually have left to work with after the key deductions are done.

Want to see your own likely proceeds worked out properly — including CPF refund, outstanding loan, and estimated cash in hand?

Request a seller reviewThese figures are illustrative and opinion-based, produced with calculation tools — not a valuation or financial advice. Human error is possible; verify against official sources before relying on them.

Common Mistakes HDB Sellers Make

A Simple Framework to Help You Decide Whether To Sell Your HDB

Sell now

- your next move is financially workable

- you understand your likely take-home proceeds clearly

- the move serves a real life need or strategic housing goal

- waiting is unlikely to improve your outcome meaningfully

- you are acting from readiness, not emotion

Prepare first

- the move may make sense, but your numbers are not yet fully clear

- you need time to prepare the flat, tighten the sequence, or understand the next purchase better

- you want to move, but the plan still needs more structure before you commit

Wait and review later

- your next move is still unclear

- the sale would leave you in a weaker or more pressured position

- the decision is being driven by temporary noise rather than long-term logic

- your own finances, family plans, or timeline suggest that a later review would be more sensible

What Happens After You Sell: The Transition You Should Plan For

About the author

Rick Long is an Associate Senior Division Director at Huttons Asia.

Through YouHome.sg — Right Property Matters — he shares the frameworks, tools and field experience behind his advisory work, helping Singapore buyers and sellers across HDB, EC and private residential decisions with structured, calm, next-step guidance.

CEA Reg. R026818Z · Huttons Asia · YouHome.sg

For more Singapore property planning tips, follow me on Instagram.

Your support means a lot.

Frequently Asked Questions About Selling Your HDB

Questions HDB Sellers Commonly Ask

These are some of the most common questions homeowners ask when deciding whether to sell now or wait.

How much cash will I actually get after selling my HDB? +

Are HDB resale prices falling? +

Will waiting get me a higher price for my HDB? +

How does CPF refund affect my sale proceeds? +

Should I sell my HDB before buying my next home? +

Does my flat's remaining lease affect whether I should sell now? +

Does the removal of the 15-month wait-out period affect me as a seller? +

What if I'm just exploring and not ready to sell? +

Want to understand what these questions look like with your own numbers and next-move plans?

Request a seller reviewDeciding Your Next Step as an HDB Seller

The smartest next step is rarely to rush into the market — or to delay by default.

It is to understand whether the move actually works, not just whether the price sounds right.

That means your likely take-home proceeds, your CPF refund, the real cost of the next home, and whether the move leaves you with more room or less.

Because a good sale is not judged by price. It is judged by what it lets you do next — and whether that next step feels workable for the life you are building.

You've thought it through. What an article can't do is tell you what your flat would realistically fetch, what the CPF refund takes back, and whether the move leaves your family better placed. One session with Rick closes that gap.

✓ Article read — you've done the groundwork.

Rick will confirm the session with you directly on WhatsApp.

If WhatsApp didn't open, tap here

This sends a session request via your own WhatsApp — Rick confirms the timing and meeting place with you personally. Nothing is stored on this page.

Disclaimer: The case studies and information are for educational use only, and I make no representations or guarantees with respect to the accuracy, applicability, or completeness of the contents.

There shall be no liability for any loss or expense whatsoever relating to property or investment decisions made by the reader.

What My Clients Say | Genuine Experiences

Real stories, real experiences—because your journey deserves nothing less than the best.

Awards and Accolades