Five years ago, you turned a key.

It wasn’t just a door you opened — it was a chapter.

A subsidised entry into Singapore’s private market, with rules to follow and equity to build while life unfolded.

Now, your Executive Condominium has reached its Minimum Occupation Period (MOP) — and something fundamental has shifted.

You can sell to Citizens and PRs, rent it freely, or plan your next move to fit the life you’re building.

Most owners don’t feel freedom here — they feel fog.

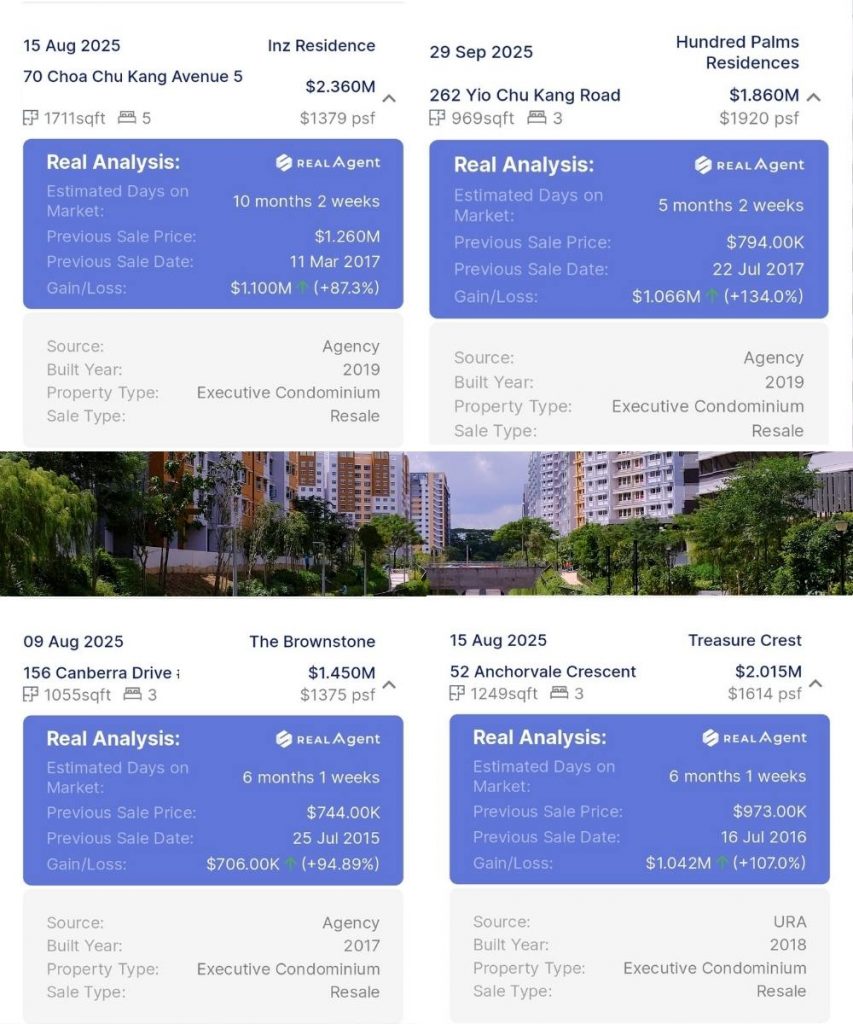

The numbers are real (loan balance, CPF refund with interest, stamp duties).

The options are many. The stakes are high.

This guide clears that fog.

You’ll see how policy, finance, and timing intersect; the four main paths EC owners take after MOP; and the interactive tools to model your own position before acting.

Our aim isn’t to sell you a strategy — it’s to give you a system that reveals what’s possible, and when.

This guide breaks that complexity into a sequence of clear frameworks.

You’ll see how policy, finance, and market data converge — and how each path affects your liquidity, loan eligibility, and long-term property plan.

Throughout the article, we will help you map your own scenario and visualise outcomes before taking your next step.

At YouHome.sg, our objective is simple: equip every EC owner with precise information and structured options.

Because smart property moves aren’t made through guesswork — they’re made through systems that show you what’s possible, and when

With the current situation. Whats your take on moving forward. My unit is going MOP soon. Have not decided if i should sell

Hi Mr Chan. thanks for reading our article. I would suggest assessing your current situation/life stage. Understand your priority in moving forward. We would work out the financial calculation with you and see the options available.

Thank you for the information. For option 2 – sell EC buy resale HDB – am I able to buy a resale hdb first then sell my EC? What is the time frame?

Hi Jenny,

Yes you can purchase a resale Hdb 1st. Time frame is 6month to sell after completion of the Hdb.